Farmer sentiment improves; less pessimism over interest rates

James Mintert and Michael Langemeier, Purdue Center for Commercial Agriculture

A breakdown on the Purdue/CME Group Ag Economy Barometer April results can be viewed at https://purdue.ag/barometervideo. Find the audio podcast discussion for insight on this month’s sentiment at https://purdue.ag/agcast.

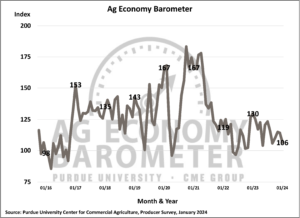

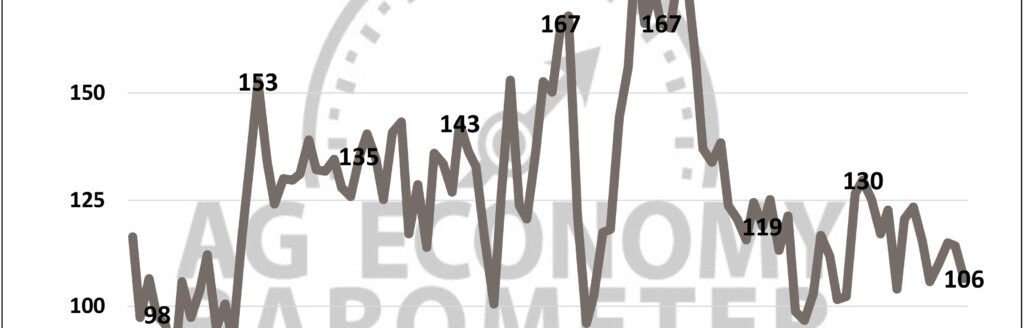

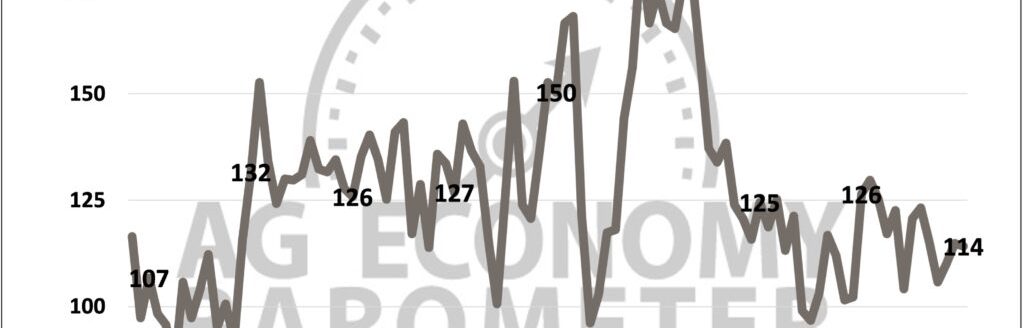

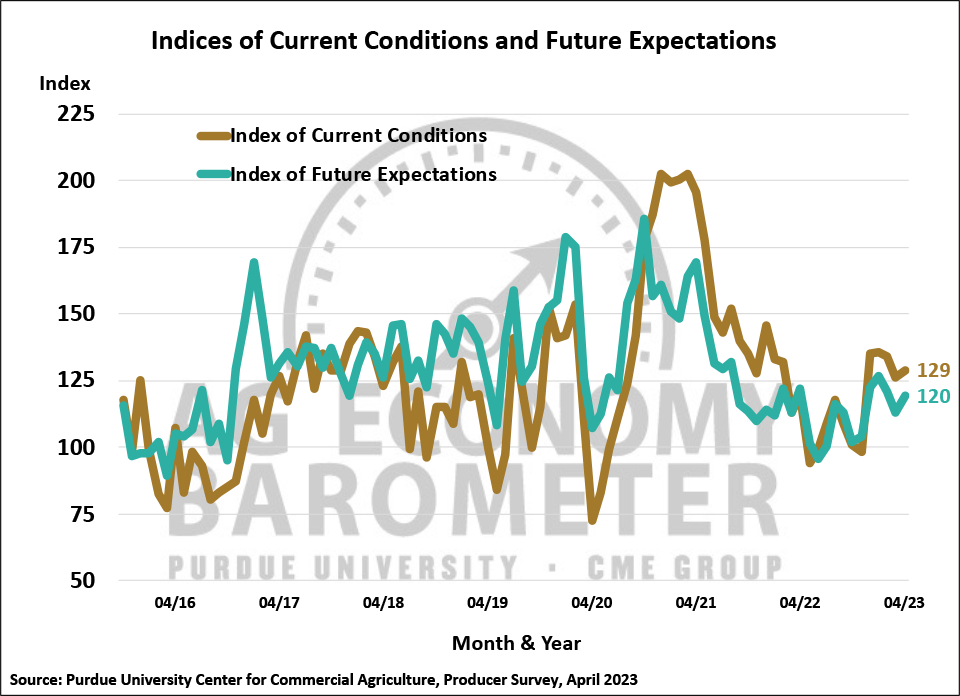

Farmer sentiment improved modestly in April as the Purdue University-CME Group Ag Economy Barometer reversed a two-month decline up 6 points to a reading of 123. Both the Index of Current Conditions and the Index of Future Expectations improved in April with the biggest rise taking place in future expectations. The Current Conditions Indexrose 3 points to 129 while the Index of Future Expectations rose 7 points to 120. When asked to look ahead one year, more producers said they expect to be better off financially than now with fewer respondents expecting conditions to worsen compared to both a month earlier and one year earlier. This month’s survey was conducted from April 10-14, 2023.

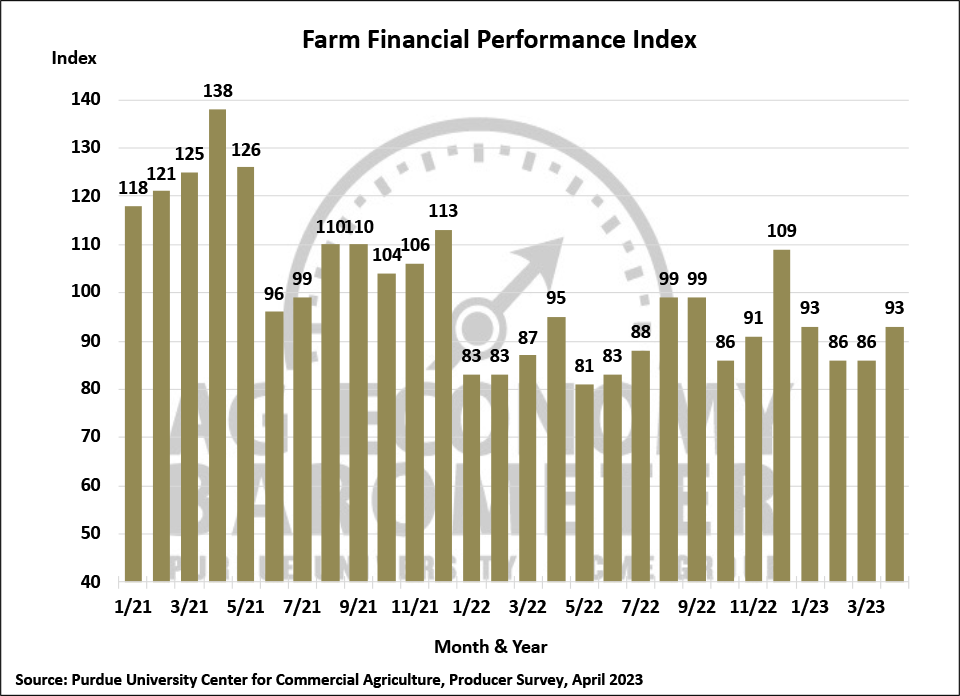

The Farm Financial Performance Index rose 7 points in April to 93, matching the index’s January reading. The prime interest rate charged by U.S. commercial banks increased from 7.75% in January to 8% in late March and a shift in farmers’ expectations regarding future Federal Reserve Board interest rate policy could be one reason the financial performance index improved this month. Compared to earlier in the year, fewer producers expect interest rates to rise over the next year and more producers think rates are likely to hold steady or even decline. This month 34% of respondents said they expect the U.S. prime interest rate to remain unchanged or decline over the next year compared to 25% of producers who felt that way in February. At the same time, two-thirds (66%) of producers expect interest rates to keep rising, compared to 75% of respondents who felt that way in February. The biggest shift was among respondents expecting rates to rise 1 to 2% in the next year which declined to 37% of respondents in April vs. 43% of respondents in February.

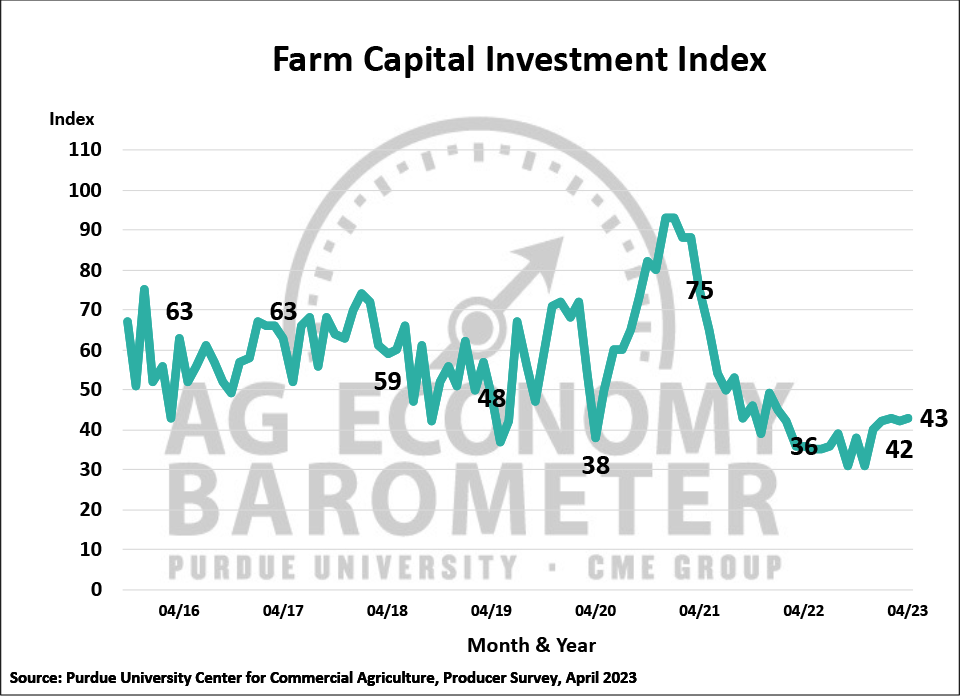

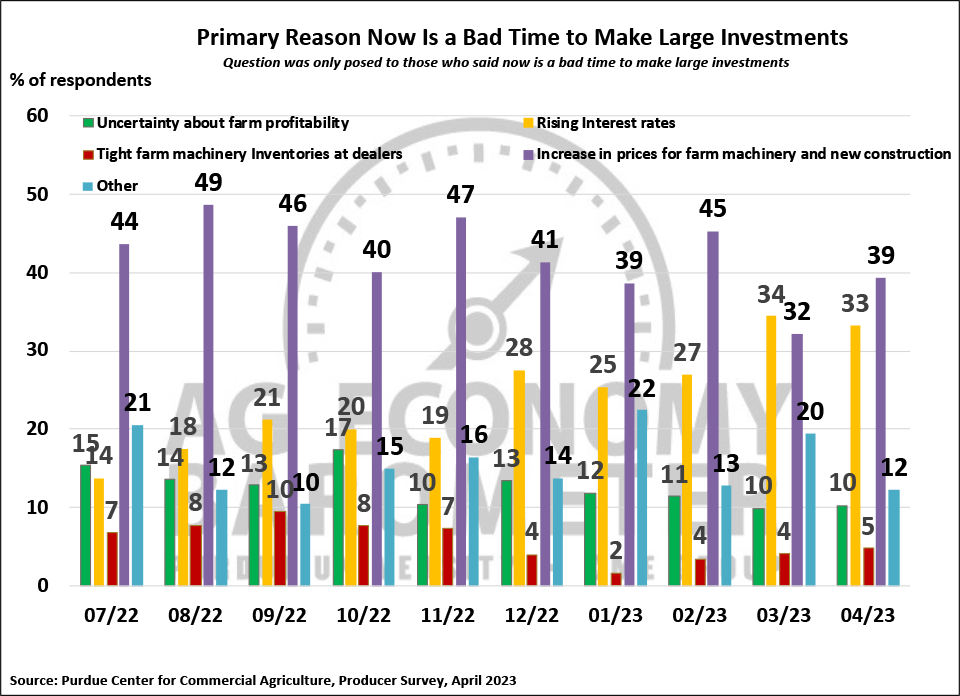

The Farm Capital Investment Index was virtually unchanged in April at a reading of 43, which was just one point higher than a month earlier. That leaves the index 7 points higher than a year earlier, but still down 32 points compared to two years ago. Among the over 70 percent of respondents who continue to think it’s a bad time for large investments, the top two reasons cited continue to be the increase in prices for machinery and construction and rising interest rates. In a reversal from last month, more respondents chose rising equipment and construction costs (39%) than rising interest rates (33%) as a top reason for this being a poor time for large investments.

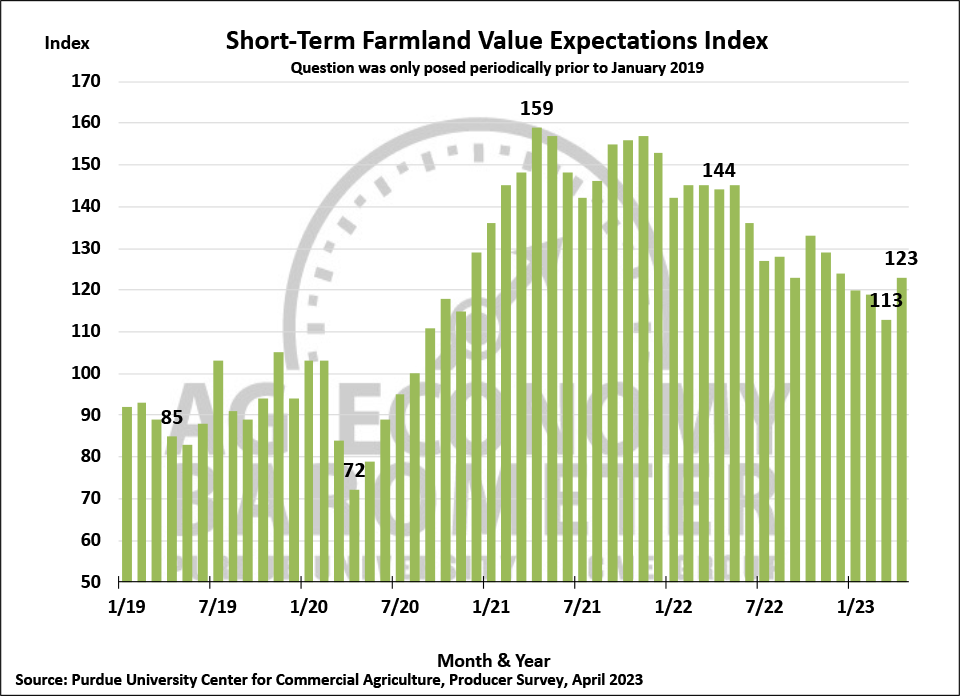

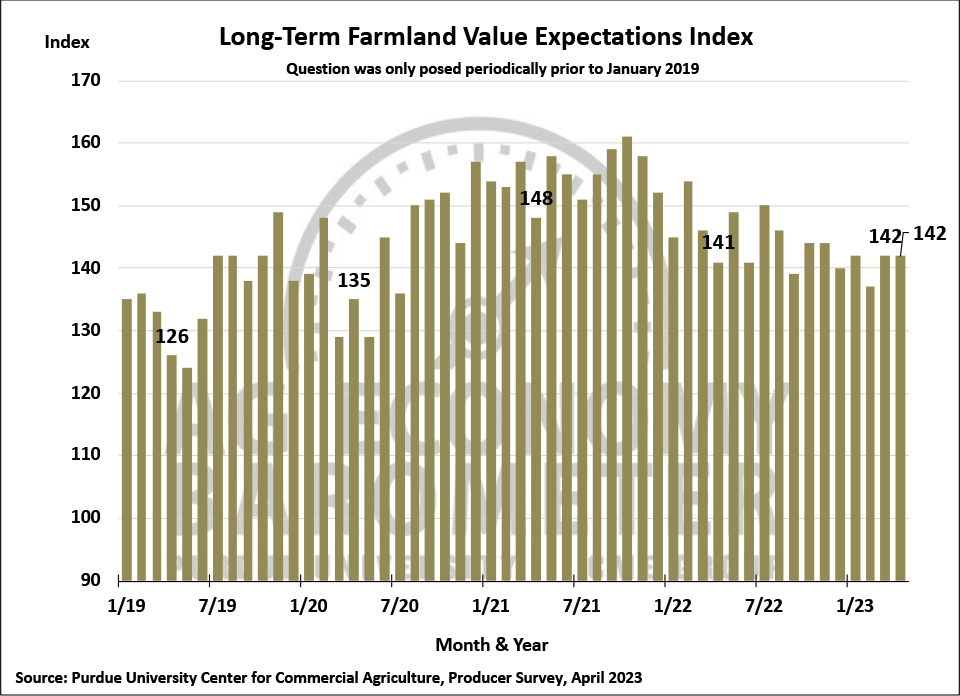

For the first time since last fall, the Short-Term Farmland Value Expectations Index increased compared to a month earlier. The index rose 10 points in April to a reading of 123 while the long-term farmland index held steady at a reading of 142. Even with this month’s rise, the short-term index remains 21 points lower than a year earlier and 36 points lower than two years ago. The shift in the short-term index took place mostly because the percentage of respondents expecting values to decline in the year ahead fell to 14% this month, erasing last month’s 6 percentage point rise in respondents expecting to see a decline in farmland values. At the same time, the percentage of farmers who expect values to rise in the upcoming year rose from 33% to 37% this month. A less pessimistic prime interest rate outlook among producers could help explain the improvement in the short-term outlook for farmland values among producers.

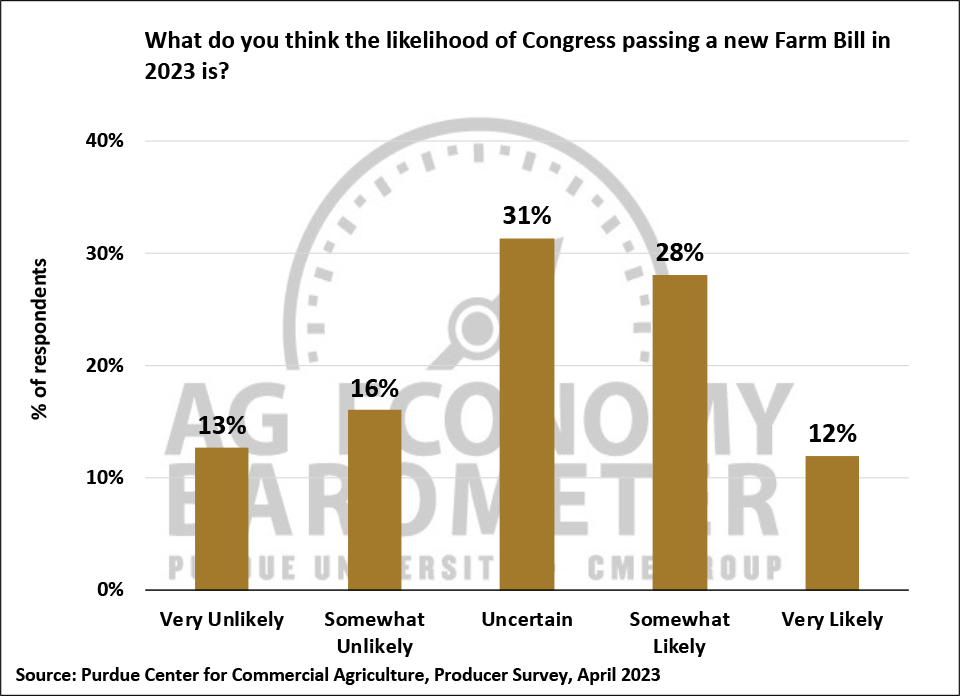

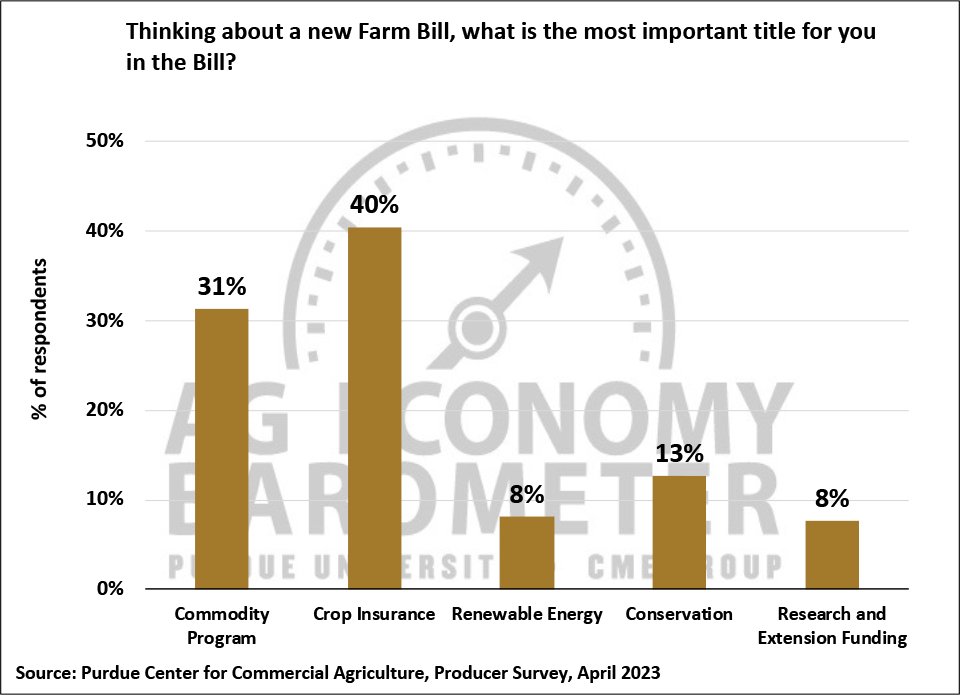

Farm Bill discussions are heating up and this month’s survey included a couple of questions to learn more about producers’ perspectives on Farm Bill legislation. Opinions on the likelihood of a new Farm Bill’s passage before the end of the year are divided. Four out of 10 (40%) of producers think that passage of a new Farm Bill this year is either very likely (12%) or at least somewhat likely (28%). But on the other side of the coin, 29% of producers think that the Bill’s passage is either very unlikely (13%) or somewhat unlikely (16%). The survey queried corn and soybean producers regarding what they consider to be the most important aspect of a new Farm Bill to them. Forty percent of respondents chose crop insurance as the most important Farm Bill title, followed by the commodity programs (31%) and conservation titles (13%). The research and extension and renewable energy funding titles were each chosen by 8% of respondents as a top priority.

Leasing farmland for solar energy production continues to be a hot topic in some parts of the U.S. In this month’s survey, 15% of respondents said that, in the last 6 months, they had actively engaged in discussions with companies about leasing farmland for solar energy production. Following up with just those producers who had been discussing solar leasing with a company revealed an upward shift in the long-term lease rates being offered to lease farmland with nearly half of the respondents indicating that lease rates of $1,000 or more per acre were discussed. In particular, 25% of respondents said that, following the development and construction period, the lease rate they were offered was $1,250 or more per acre while 22% of respondents said the lease rate they were offered ranged from $1,000 up to $1,250 per acre. On the other end of the spectrum, 32% of respondents said they were offered lease rates of less than $500 per acre. Fewer producers reported receiving offers ranging from $500 up to $1,000 per acre than in previous surveys.

Wrapping Up

Farmer sentiment improved in April with a more optimistic view of the future being the biggest driver behind the sentiment shift. More producers expect prime interest rates to either hold steady or possibly decline during the next 12 months than felt that way earlier in the year. Producers’ perspective on farmland values shifted somewhat in April with fewer producers expecting values to decline in the upcoming year and more producers looking for values to rise than a month earlier. When asked about the possibility of a new Farm Bill being passed by Congress in 2023, responses were mixed with 40% of producers saying that passage was at least somewhat likely while nearly 30% of respondents think that passage is at least somewhat unlikely.

The post Farmer sentiment improves; less pessimism over interest rates appeared first on Ag Economy Barometer.