Spring has a way of quickening the pulse on the High Plains. As the days stretch and fields shed their winter chill, farmers itch to roll planters out of the shed.

But this season, before seed hits the furrow, many will give their spreadsheets and risk plans one more hard look. It is not hesitation, it is strategy. Economics are in the cab right alongside agronomy, and together they are steering a cautious approach to 2026.

The crop-planting merry‑go‑round

Acreage conversations have already started their annual spin. Early estimates from analysts and the U.S. Department of Agriculture’s Ag Outlook Forum point to corn acres easing off last year’s near‑record levels, soybeans clawing back some ground, and wheat slipping slightly.

The story beneath those numbers is straightforward: Rotation still matters, but the math matters more right now. Farmers who would ordinarily keep a steady corn–soy rotation are sharpening their pencils as price spreads and cost structures push the calculus toward soybeans.

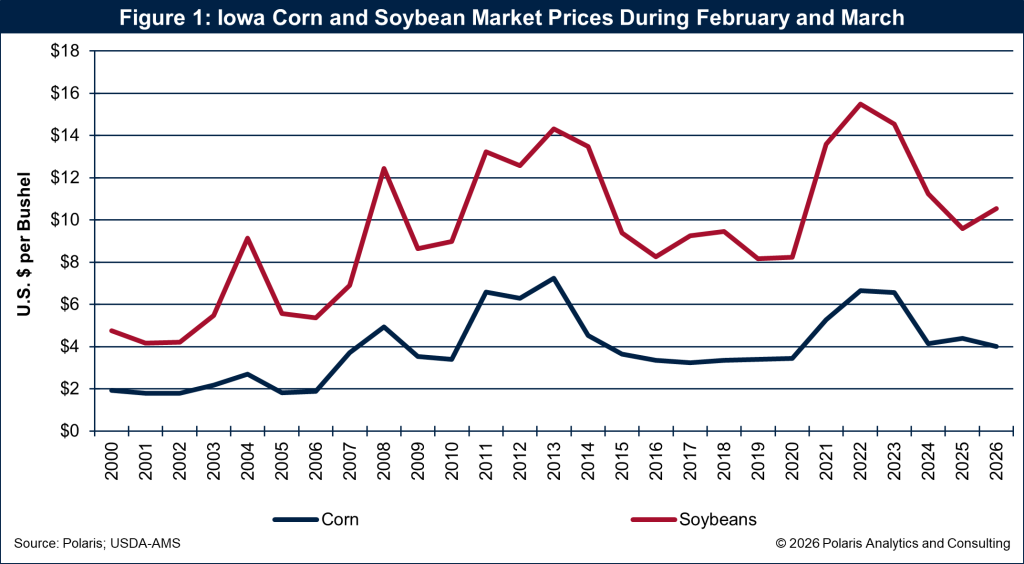

The February to March decision window is revealing. Cash corn has been hanging near the low‑$4s per bushel in many areas while soybeans have traded roughly a dollar higher than a year ago in several Midwestern cash markets.

That widening corn–soybean spread does two things. First, it pulls marginal corn acres toward beans where rotations allow. Second, it nudges producers to rethink fertilizer and chemical spend on fields likely to stay in corn, especially where yield risk is elevated.

The recent corn and soybean price relationship is shown in Figure 1 during this critical decision period, which is often as influential as any agronomic factor in determining final planting mix.

Of course, intentions are not acres. The late‑March USDA Prospective Plantings report has a way of resetting expectations as growers lock in input purchases, crop insurance and early delivery commitments. Weather can shuffle the deck, too, particularly where soil temperatures lag or spring moisture keeps heavy planters idle.

Planting pace: Time is a strategy

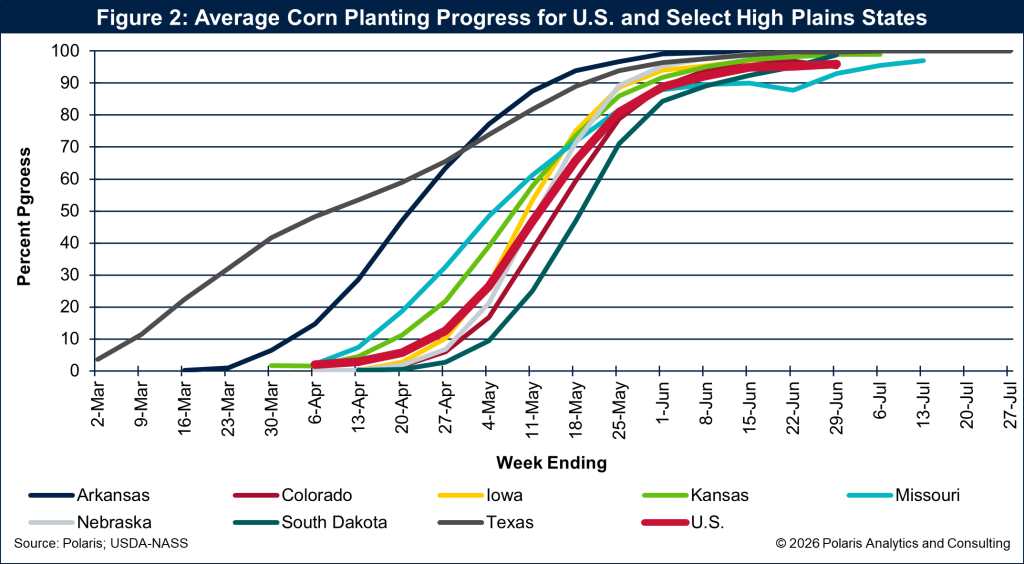

One reason caution can be a winning strategy in 2026 is time. Corn planting on the High Plains effectively runs from early March in Texas through April elsewhere and can stretch more than 10 weeks before the last planter stops in the northern fringe. Texas tends to start first and finish last, while states to the north compress more activity into a shorter window. The average corn planting pace across key states is shown in Figure 2.

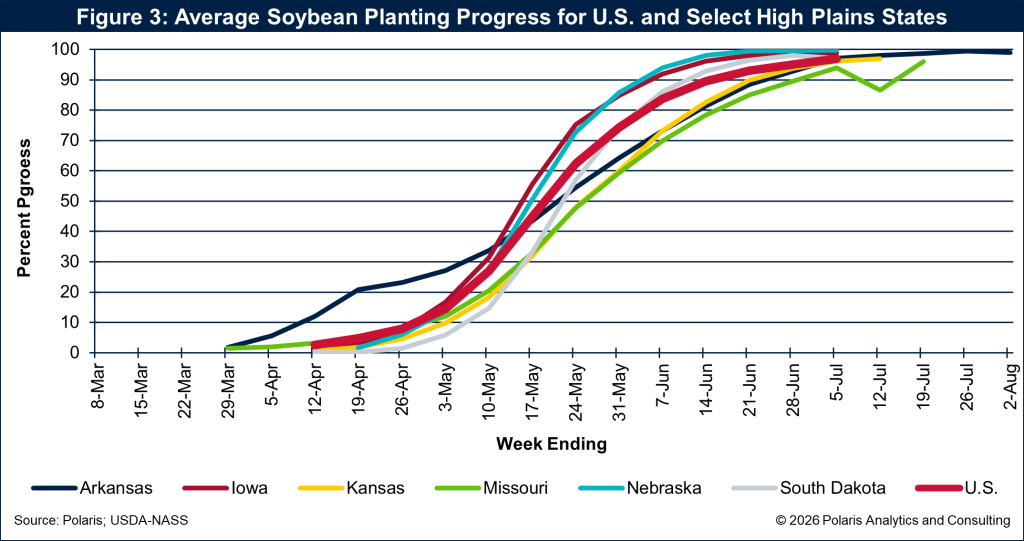

Soybeans move faster. In Arkansas and Missouri, soybeans can get underway by late March, and by mid‑May some states often have half the crop in. That sharper curve gives producers a little more flexibility to adjust acres late if prices or field conditions shift.

The soybean planting pace for the region is shown in Figure 3, and it highlights a practical advantage this spring: when economics favor soybeans, farmers can lean into that decision later in the season without ceding too much yield potential.

What these pace curves really underscore is option value. With a longer planting runway for corn and a quicker execution for soybeans, producers can fine‑tune the mix in real time, field by field, week by week, based on evolving markets, soil temperatures, and moisture profiles.

Costs, revenues, and the caution flag

Flexibility in the calendar is welcome, but the budget still has the loudest voice. Production costs in 2026 remain elevated, even if some input prices have cooled off from peaks. For many operations, corn pencils in around $900 to $920 per acre, driven by fertilizer, seed traits, fuel, and machinery overhead.

Soybeans generally land in the $650 to $680 per‑acre range, and wheat tallies closer to $400 to $500 depending on location and practice. These are ballpark figures, but they capture the spread most growers are seeing this winter.

On the revenue side, corn in the low‑$4s per bushel is a tough slog against that cost base, especially after layering in land costs and overhead. Soybeans in the $10.70 to $11.50 per bushel range offer better relative returns, buoyed by steady crush demand and biofuel pull‑through, though basis and protein discounts still matter locally.

Wheat remains soft, which complicates rotations where wheat is the agronomic anchor. The result: Net returns on corn look marginal to negative for many fields, while soybeans present a measurable buffer, particularly on acres with average yield potential.

Crop insurance ties directly into the risk math. With February price discovery setting revenue guarantees, lower futures prices translate into lower protection levels unless producers opt for higher coverage bands. That puts more weight on marketing discipline (spreads, basis management and new‑crop hedges) and input timing (particularly fertilizer buys) to defend margins. In short: 2026 is not the year to chase acres; it is the year to protect working capital and prioritize risk‑adjusted return.

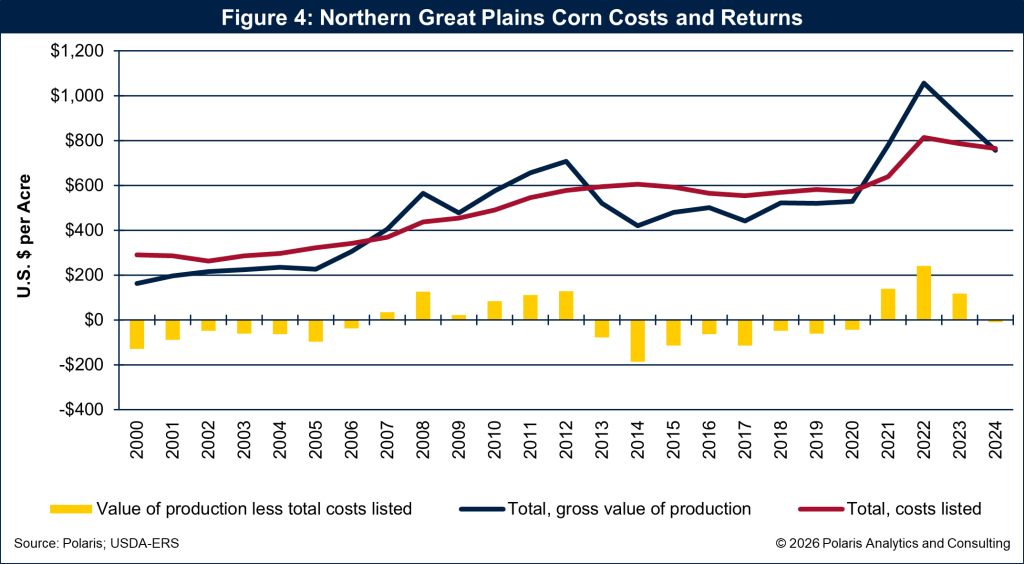

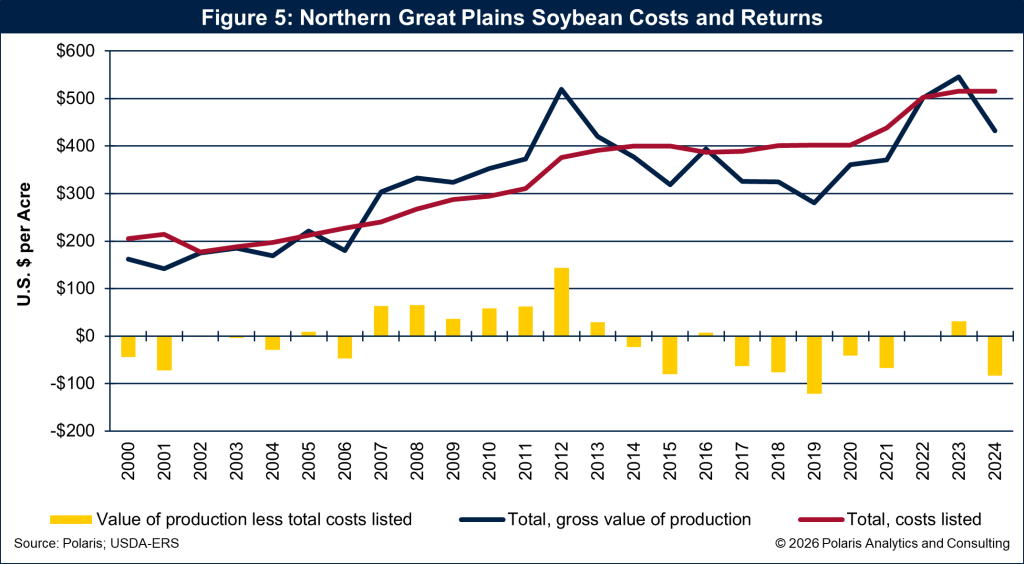

A long‑view perspective helps. Figure 4 tracks historical corn gross value, costs and net returns while Figure 5 tracks soybeans. It is a reminder that agriculture’s profit cycles are real, and they turn. When returns compress, the operations that endure are typically the ones that match crop choices to cost structure, protect balance sheets, and avoid letting short‑term price rallies dictate long‑term risk.

What caution looks like in the field

Caution is not about parking the planter. It is about sequencing choices, so each decision keeps more doors open than it closes.

- Rotation first, then arithmetic. Healthy soils remain the foundation of profitable farming. Where rotations are flexible, let the numbers nudge acres toward soybeans; where rotations are tight, refine the corn plan with input efficiency and realistic yield targets.

- Stage decisions with the calendar. Use the early‑start regions to lock in “must‑plant” acres, then keep swing acres nimble. The pace data suggest there is room to adjust—especially into soybeans—if prices or weather change.

- Right‑size risk tools. Align insurance coverage with cash‑flow needs and be explicit about the role of pre‑harvest sales. Deep out‑of‑the‑money calls or put floors can add asymmetric protection if volatility ticks up.

- Watch basis and logistics. With burdensome old‑crop stocks in some corridors and ample global supply, basis may do more of the heavy lifting on revenue than flat price in 2026. Firm delivery plans and storage strategies reduce unpleasant surprises.

Planting ahead—with eyes wide open

The impulse to go full‑throttle when spring arrives is part of who farmers are, but this season, “Caution: Planting Ahead” is not a warning sign, it is a plan. The market is asking growers to be deliberate: to let agronomy guide the field map, let economics decide the swing acres, and let risk tools carry the load when weather or prices do not cooperate.

There is still time to shape 2026. The planting window is wide enough, the soybean‑corn spread is sending a clear signal, and the budget math is frank about what it will take to be in the black. Farmers will do what they always do, adapt. That means planting, growing, and marketing with discipline, keeping an eye on cash flow, and making sure every pass across the field earns its keep.

Caution is not a pause. It is purpose. And this spring, purpose is the smartest thing you can plant.

Ken Eriksen can be reached at [email protected].