Cozzens gives economic analysis for livestock, feed sectors during CSU webinar

Several factors are driving livestock and feed sectors in Colorado and across the United States, Tyler Cozzens, director and agricultural economist at the Livestock Marketing Information Center, told attendees during a recent webinar.

Many producers are making critical decisions about possible drought conditions, small cow herd numbers with less incentive to rebuild herd numbers. As an agricultural economist, Cozzens wanted to keep more of a perspective from feed impacts to markets, livestock and crops.

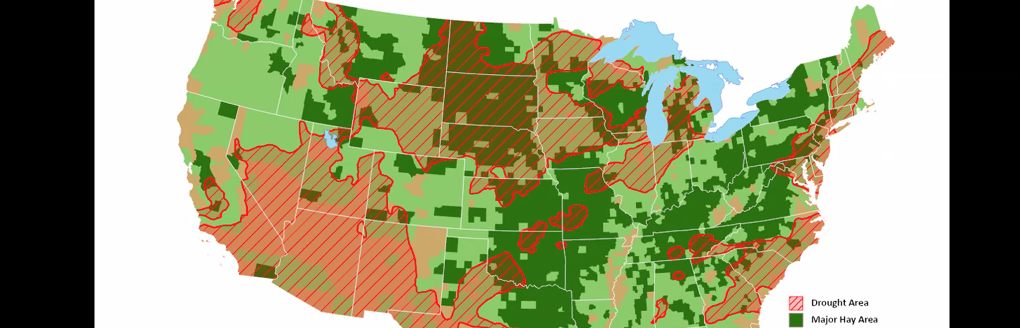

Weather plays a role as there are areas of drought spread across the Pacific Northwest, Montana, parts of the southwest, Texas, and the Corn Belt. The snowpack level is concerning from a feed standpoint.

Feed availability

Overall feed availability is being impacted in the western U.S. by a lack of moisture and water and that weighs on livestock production.

Hay producing areas aren’t immune to drought and dryness, and Cozzens is concerned about areas of Texas, Oklahoma, Arkansas, Missouri, and other regions. Many producers won’t have a good idea about hay supplies until spring growth startsstarts, and they can stop feeding as much hay.

“If you kind of want to guesstimate and overlay some of this drought with some of these major hay producing areas, there’s probably going to be some impact there,” he said.

The U.S. Department of Agriculture reports about 46% of hay acreage has been in regions experiencing drought, he said.

Fortunately, in Colorado, the hay stocks are some of the highest the state has seen in roughly three or four years.

“But as we’ve seen, some of that higher inventory level—that definitely has pulled the price of hay down,” he said adding prices are at a decade low.

When it comes to corn, there is drought pressure in and around the Corn Belt, and even though spring planting hasn’t started yet for 2026, producers are already starting to make planting decisions.

Seeing drought persisting in the Corn Belt area, particularly in parts of Nebraska is concerning, he said.

He believes the cattle feeding sector might be impacted with less corn available because of drought. The 2025 corn crop was one of the largest on record.

“And current forecasts from USDA are expecting another large corn crop here in the next crop year,” he said. “So definitely larger supplies are weighing on those prices, keeping them kind of that expectation around that $4 (a bushel) mark.”

In Colorado, corn prices tend to be a little bit higher; at least they have been in the last five or six years, but still in that $4 range, he said.

“If you’re livestock producer, feed cost side of things, definitely seeing feed costs that are probably going to be pretty similar to what you saw a year ago, but you know, we’re only two months into this year, so definitely a lot of factors at play that could still influence the overall price for corn as we move through the growing season,” Cozzens said.

Moving on to the cattle supply side, Cozzens said the cowherd numbers are still at the lowest level in roughly 75 years.

“Our economic theory says if supply goes down, all else equal, prices go up, right?” he said. “That’s what we’re seeing happen. Prices increasing in roughly the last four years. As supplies are definitely starting to tighten, we’re seeing that price response start to move a little bit higher as supplies that have gotten smaller.”

He expects pretty strong prices in 2026, and he bases it on strong demand.

Drought is also pressuring cattle producers, and prolonged drought in some areas where farms and ranches are located—Nebraska, Oklahoma, and parts of Texas—is one factor keeping inventory levels where they’re at.

“USDA is saying that approximately 34% of the cattle inventory is within an area experiencing drought,” he said.

According to Cozzens, many of the U.S. agricultural economists know that herd rebuilding is difficult to project because of the extensive drought pressure across the country. That starts to raise the question if there will be much rebuilding in the next two years.

That has meant a more measured approach to production in the future, as producers trying to make some of these decisions, he said.

Many producers are trying to see if they have the feed resources available to rebuild the herd or if they’ll have to purchase supplemental feed, he said. The cost of that feed will play a huge role, and if it’s available locally or if it will have to be shipped in.

Cattle of feed numbers reflect the smaller herd numbers, with about 11.5 million head of cattle on feed according to USDA, Cozzens said.

“Compared to a year ago, we’re down quite a bit and even the five-year average,” he said. “This is a trend that’s been going on for last couple of years, just lower number of cattle on feed, and likely to persist through this year, really won’t see much gain in overall number of cattle, least in ‘26 and likely ‘27.”

Cattle are also starting to stay on feed longer, and since 2024, some are pushing past 150 days on feed. Cozzens said this is pushed largely by the cheaper feed costs for corn and hay,

There is marginal cost and marginal gain associated with feeding cattle longer, and every feed operator knows his breakeven point.

The result of cattle staying on feed longer means larger finished weights. Many packers are seeing dressed steer weights nearing 1,000 pounds in the 908- to 990-pound range.

“This is well above what we saw last year, well above the five-year average,” Cozzens said. “This is probably a trend that’s not going to change much.”

He believes dress weights will stay above 2025 levels, and this will help maximize cattle and get as much beef from each steer or heifer that’s in the feedyards.

“As a result of getting a little bit more weight on them, on feed a little bit longer, what we’re actually seeing is from a grading standpoint we’re seeing a lot of these carcasses grade Choice, high Choice and Prime,” he said. “We’re seeing fewer number of cattle grades Select.”

This pushes consumers’ overall eating experience at the retail level.

“Consumers are getting a better-quality product at the store, and they’re showing up and paying for it,” Cozzens said. “There’s a lot of factors kind of at play here, but we’re seeing quite a bit of higher quality product and that kind of starts to shape the overall demand profile from a consumer standpoint. The consumers are showing up and it’s a very good sign for the cattle feeding sector, especially given the prices that we’re seeing as well, too.”

As for slaughter, Cozzens isn’t expecting to see many more head come through packers than it did in 2025. He believes 2026 and 2027 will be similar.

“They’re offsetting part of this with just overall larger dress weights to keep the overall beef production higher,” he said. “The number of head that are coming through is still not offset, not able to keep up with the overall beef production that we typically have seen, and largely with the beef production that we need to keep up with the domestic demand that we have here.”

He sees a transitionary stage in the next year or two until there can be more hooves on the ground and supplies moving through the supply chain.

Trade

There’s been a lot of discussion around the New World screwworm and how it’s affecting imports of Mexican cattle. That’s basically been on hold since May 2025.

“We were importing about a million head of cattle from Mexico,” he said. “You can’t think about the overall supply picture—then you take a million head of cattle out of that picture it definitely impacts the overall supply availability within the U.S., not having those cattle come from Mexico.”

Looking at beef imports, Cozzens found a couple things after looking at the 2025 data. Australia was the main supplier of beef in 2025, and that’s not surprising, he said. It was a 27% increase from 2024 to 2025.

“This is kind of been one of those trends that’s been occurring for a number of years now. Australia is definitely one of those suppliers globally that actively looks to get as much beef into the U.S. market, as much as they can,” he said.

After Australia, Canada came in second, Brazil third, Mexico fourth and New Zealand rounding out the top five. Cozzens noted Argentina wasn’t in the top 5.

“Argentina has definitely been one that’s popped up in the news quite a bit,” he said. “What I will note, as far as a market share of the beef that we imported in 2025, 2% of the beef that we imported came from Argentina.”

He’s received many questions about the impact of importing beef from Argentina, and he said even if you double what they’ve sent here, it’s really not going to make an impact on prices. He’s more concerned with the shares from other countries, and even though live imports of beef aren’t making their way to the U.S., he does believe there’s more coming across the border in a box.

Exports

“Obviously, with the tighter domestic supplies, lower beef production means lower beef exportable supplies to the global market,” he said. “Beef exports were down 14% in 2025 compared to 2024. A lot of that decline across the board.”

South Korea stayed about even from 2024 to 2025, while other major trading partners—Japan, Mexico, Canada, and Taiwan were all down in that time frame.

“This is probably going to continue in 2026 and probably 2027 just lower exportable supplies, higher price, definitely a headwind to just overall exports,” Cozzens said. “But for me, looking at exports, South Korea and Japan are major destinations for overall beef exports. So, maintaining some market share there is definitely key for the U.S., from an export standpoint, and just price support for domestic beef prices.”

Cattle prices

As for cattle prices in Colorado, Cozzens pulled some prices for the state and said when looking at cull cow prices, the average dressing breaking prices; he made a couple of assumptions. First, a 1,500-pound cull cow brought nearly $2,500 in the first couple of months of 2026.

A year ago, the prices were lower and the five-year average was even lower. Thus, the cull cow demand is quite strong, and it’s driving demand for ground beef product.

“That 80% lean product to be ground with more fat trimmings that we’re getting from just those higher dressed weights make a little bit more ground beef for these consumers still demanding beef, burgers and things fast food restaurants and just grilling,” he said.

That gets a little concerning from a rebuilding standpoint if the cull cows are so valuable.

“Is there much incentive to retain some of these cows and really actively rebuild herd?” Cozzens said. “And that’s different for every operation. But I just bring this in for discussion point. From just purely an economic standpoint, just economic drivers within the cattle market.”

Colorado steer calf prices are strong too.

“You’re looking at $2,750 per head for these feeder steers, well above prices that we were seeing a year ago, well above the five-year average,” he said. “So definitely some very strong prices.”

A stronger argument can be made for more upside potential for prices than what the future expectations are, but he believes prices will likely be above a year ago levels going through 2026.

“A lot of this will hinge on just overall demand remaining strong from the consumer for beef,” Cozzens said.

Kylene Scott can be reached at 620-227-1804 or [email protected].