Look at the bigger picture for livestock, economy

Tyler Cozzens, director of the Livestock Marketing Information Center, provided his outlook on livestock and crops both nationally and in Colorado at the recent Colorado State University Livestock & Forage Growers Update.

Cozzens provides economic analysis for the livestock and feed sectors at LMIC and analyzes the bigger picture about the economy, large factors playing into it, and how demand is shaped. At the time of the webinar, the Consumer Price Index had just been updated, and he said there was a 2.8% increase in the overall CPI. This index excludes more volatile goods—like food and energy.

“As far as inflationary pressures go, definitely an improvement of where we were two to three years ago,” he said.

Back then inflation was ranging from 4 to 8%, but the economy is still dealing with lingering effects.

Non-housing debt balance and credit card debt are a couple of household items Cozzens monitors. Credit card debt at the end of 2024 was more than $2.1 trillion, a record high and that margin during the last 10 years has started to widen.

“It’s definitely one of those that you look at as far as just from a larger economy standpoint of consumers,” he said. “Are they putting more purchases on that credit card? What purchases are they putting on that and are they able to repay that credit card at the end of the month? And I would argue some of this stems from just the overall inflation that we saw a couple of years ago.”

He hopes consumers can pay down their debt and “still maintain some of their purchasing power on a larger scale,” he said. “It’s important to recognize the overall purchasing power of the consumer and how they spur on the economy.”

Agricultural economy

For the agricultural and livestock sector, Cozzens starts with interest rates. Those have “definitely increased over that 5% rate over the last few months and years,” he said. Cozzens often observes the feeder cattle variable interest rates from Dallas and operating loan rates from Kansas City. These two items often have a similar trend to what the Fed fund rate is reporting.

“The thing I want to point out is we’re sitting at a variable interest rate for these operating loans versus feeder cattle that is just above 8%,” he said. “So, we compare that to roughly a decade ago, you can see that 3 to 4 percentage point increase.”

A decade ago was the last time there was a significant herd rebuilding effort.

It’s also costing producers more to do business.

“That borrowing capital from a bank is higher than it was a decade ago, and so definitely a headwind to the overall ability of the producer to start expanding their operation, if they want to, or just borrow capital,” Cozzens said. “This isn’t something that is unique to just the agricultural industry or livestock sector. This goes across the economy as a whole. The interest rate is kind of one of those levers that’s pretty easy for us to use to throttle the economy.”

Hay

Looking at the forage, Cozzens looked at United States total hay stocks and when he peeked at the Dec. 1 all-hay stocks, he noticed a couple of trends.

In the past couple of years he has watched the supplies grow with more production. If the demand has not changed that will move prices lower, he said. He expects hay prices will be a little bit lower nationally and in Colorado when compared to a year ago.

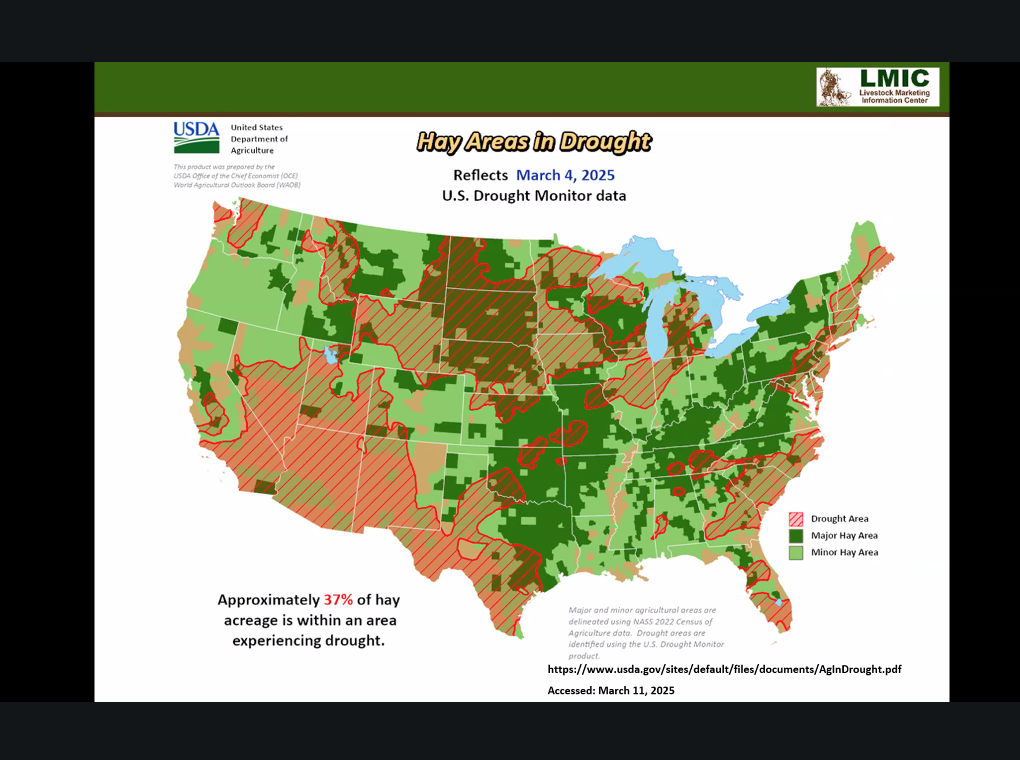

Drought and weather will play into the agricultural sector and several major crop and livestock producing regions are suffering from the lack of precipitation. Hay acres aren’t immune either.

“Approximately 37% of the hay acreage is within an area experiencing drought,” he said. “There are potentially some impacts to just overall hay production and hay supplies potentially as we get into 2025. Obviously, this is a little bit more short-term picture as we look at the drought.”

Corn

Cozzens said the U.S. Department of Agriculture announced a few weeks ago it forecasts 94 million acres of corn to be planted this year.

If the trend line toward yield growth occurs it points to higher corn supplies, he said.

That too is weighing on corn prices. There’s been several years of prices of more than $6 a bushel, but there’s expectations for lower prices this year. Colorado has had stronger prices compared to national prices, but it is trending lower.

That bodes well for livestock producers who can benefit even when compared to those costs in the past three years, he said.

Market expectations

Cozzens said Omaha corn prices best represent corn prices from a national perspective, and they’re “definitely lower than what the five-year average has been.”

“But compared to a year ago, we’re tracking slightly better to even with where we were a year ago,” he said. “The overall market expectation for corn prices moving forward in 2025 is looking to be about that $4.50 to maybe $5 mark as the current (expectation) sits right now.”

Corn hasn’t been put in the ground yet, and there are unknowns about the overall supplies moving forward, he said. Drought potential is a concern especially for northeast and eastern Colorado as well as major areas of the Corn Belt.

If drought occurs in large part of the Corn Belt that would slice yields and point toward potentially higher prices, he said.

Cattle

Inventory numbers from the USDA, National Agricultural Statistics Service released at the end of January, Cozzens said, and the biggest takeaway for him was from an overall supply picture. Overall beef cows and beef cow replacements were still down from a year ago, less than 1%.

“We’re watching those two key categories as those give us kind of our indication of overall expectations of supplies moving forward,” he said. “Seeing those down from a year ago still paints a picture that supplies are going to be tight as we move through 2025.”

Many producers have economic concerns when it comes to rebuilding the herds. Cozzens said to keep in mind the overall interest rates being offered and how that influences decision making.

“There’s some producers out there, maybe some of those smaller producers that have started to actively get a little bit more aggressive about rebuilding their herds, but the calf crop’s down slightly from a year ago,” he said.

That still points toward tight supplies going through this year. Some analysts see the potential for an increase in numbers later this year. He believes there could be an increase in numbers the closer 2026 comes.

“But I think the increase—as we get through this year and moving to 2026—is going to be modest,” he said. “I think this is going to be a very measured approach as far as the rebuilding efforts go on the cattle side of things.”

Wrap-up

Cozzens said through his discussions and talks he’s given; drought and pasture conditions continue to be one of the bigger challenges along with overall feed availability and cost.

“We have some larger looming economic issues here—geopolitical issues, inflation and trade,” he said. “I’ll just bring back the interest rate discussion. Demand held very strong here in 2024 hoping to see that continue in 2025 here, but global demand is still part of that picture.”

So are exports, as high value beef is a good portion of the beef going overseas. Exchange rates will play a role in that too.

“So just some bigger things to keep in mind and watch in the coming year,” he said.

Kylene Scott can be reached at 620-227-1804 or [email protected].

Related Articles