High Plains wheat marketing developments serve the U.S. and world

Across the High Plains, wheat producers are navigating a season defined by rapid crop development, mounting moisture stress and sharply diverging yield potential.

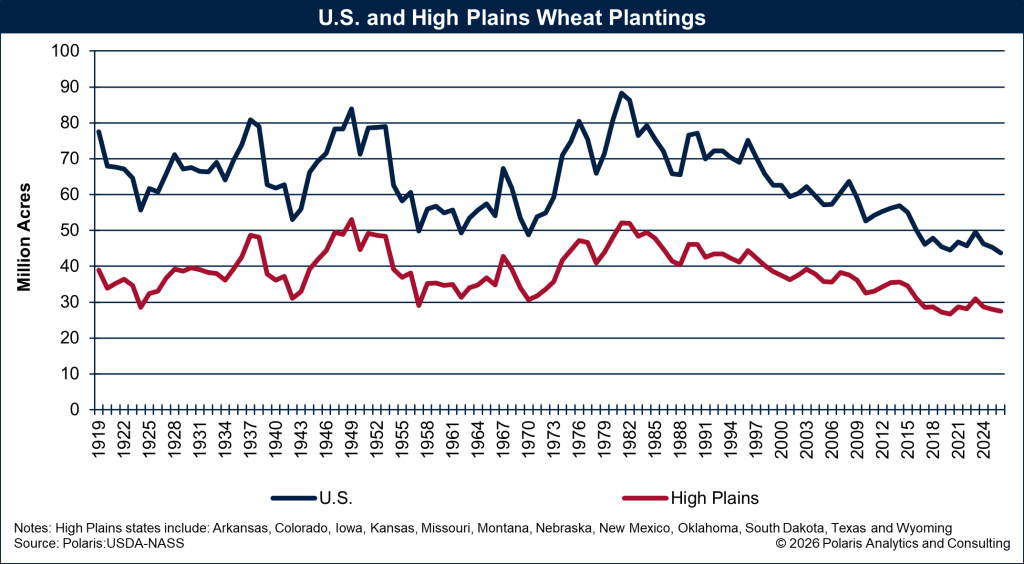

From winter wheat moving quickly through jointing in the Southern Plains to spring wheat planting in the North, wheat’s role as both a domestic staple and a global food security crop remains critical. It comes at a time when acres intended for wheat were the lowest since 1919. According to the U.S. Department of Agriculture’s Prospective Planting Report, released March 31, U.S. total planted area for wheat is projected at 43.8 million acres. Across the High Plains, wheat planted area is projected at 27.4 million acres, the lowest level since 2020.

Marketing wheat in 2026 demands sharper attention to risk management, changing demand patterns and global competition, particularly in a season where time and weather appear compressed.

As Justin Gilpin, CEO Kansas Wheat, and other market watchers note, wheat may not always command headlines like corn or soybeans, but few crops are more sensitive to weather, quality and geopolitics—or more connected to global consumers.

“Wheat doesn’t always dominate headlines, but it’s often the first crop where weather, quality and food security intersect,” Gilpin said. “When development accelerates as quickly as it has this spring, marketing risk tends to show up sooner than expected.”

Crop conditions: a patchwork across the Plains

Winter wheat conditions vary widely across the High Plains states, reflecting the region’s hallmark variability. In the Southern Plains—Texas, Oklahoma and Kansas—stand establishment has been uneven, shaped largely by fall moisture availability and winter temperature swings, including a warmer‑than‑average winter in Kansas. Fields that emerged ahead of winter generally entered dormancy in fair condition, while later‑planted or moisture‑stressed fields remain vulnerable heading into jointing.

In Kansas, rapid development has become an added concern. Much of the crop reached jointing well ahead of normal, leaving plants with less resilience if timely rains fail to materialize. Producers in the driest western areas note that without meaningful moisture soon, abandonment decisions could factor into yield outcomes later this spring.

In the central Plains, including Nebraska, Colorado and Wyoming, producers report a mixed picture. Snow cover benefited some dryland acres, but concerns linger about thin stands and plant vigor, particularly where subsoil moisture remains limited. Grazing pressure on dual‑purpose wheat has also factored into yield potential, underscoring the tradeoffs producers manage in challenging years.

Farther north, in South Dakota and Montana, attention is turning to spring wheat planting progress as soil temperatures improve. Producers are watching weather closely, balancing the push to plant early against the risk of late‑season frost and cool soils. In eastern fringe states such as Iowa, Missouri and Arkansas—where soft red winter wheat plays a more prominent role—crop conditions generally appear more stable, setting the stage for average to above‑average yield potential, if spring weather cooperates.

Spring wheat planting: Timing and quality matter

For spring wheat producers, planting pace and early‑season weather will heavily influence not just yield, but also protein levels. High‑protein spring wheat remains a key component of domestic and export milling blends, and customers increasingly reward consistency.

“Producers aren’t just growing bushels—they’re managing functional traits,” Gilpin said. “Protein, consistency and delivery timing matter more to millers than ever, especially when weather compresses the growing season.”

Planting decisions this spring are also shaped by input costs and rotation considerations. Some Northern Plains growers have modestly adjusted acreage, weighing wheat’s lower upfront costs against price uncertainty and competition from other crops.

March 1 stocks: More than a headline number

The March 1 wheat stocks report provided confirmation of comfortable overall supplies, but seasoned market participants caution against reading too much into the headline figure. Stocks data often obscures important nuances about wheat class, quality and location.

A recurring challenge in United States’ wheat markets is that not all wheat is interchangeable. Hard red winter wheat may be plentiful in aggregate, but milling‑grade wheat with desired protein and falling number specifications can be much tighter. Conversely, large inventories of lower‑quality wheat may weigh on futures while leaving local basis values firm.

“The challenge for the market isn’t total wheat stocks—it’s usable wheat,” Gilpin explains. “In years like this, where moisture stress shows up early, you can have plenty of wheat on the balance sheet and still fall short on protein, test weight or timing. That’s when basis starts telling a very different story than futures.”

This dynamic continues to support basis strength in some regions even as futures prices struggle to find sustained upside.

Domestic demand: Wheat and the protein question

One of the more intriguing developments shaping wheat demand is the continued focus on dietary protein among consumers. While low‑carb trends occasionally resurface, wheat remains an essential component of diets worldwide, particularly through bread, baked goods and noodles.

High‑protein diets have not eliminated wheat from American menus, but they have influenced how wheat is used. Bread consumption has remained relatively resilient, supported by demand for high‑quality loaves, artisan breads and products marketed for protein content. Meanwhile, some segments of pastry and snack foods have seen softer demand as consumers shift preferences.

Wheat’s role as a plant‑based protein adds complexity to the conversation. Flour millers increasingly emphasize protein content and functional characteristics rather than just volume. This benefits classes like hard red winter and hard red spring wheat when quality aligns with customer expectations.

“Wheat isn’t competing head‑to‑head with beef or chicken,” Gilpin said. “It’s complementing those diets in different forms, particularly globally.”

Export developments: Reliability is a selling point

On the global stage, U.S. wheat continues to face stiff competition, particularly from the Black Sea region. However, recent disruptions—from geopolitical tensions to logistical bottlenecks—have reinforced the value of reliability and consistency, areas where U.S. wheat often excels.

Importers increasingly look beyond price to factors such as shipment reliability, quality specifications and supplier reputation. This trend plays to the strength of High Plains producers when quality is achieved and infrastructure smoothly functions.

Different wheat classes serve different export niches. Hard red winter wheat remains a staple for bread production in many countries, while hard red spring wheat supports premium flour markets. Soft wheat finds its place in confectionery and noodle production, particularly in Asia.

“Exports don’t disappear overnight,” Gilpin said. “They shift destinations and specifications. The U.S. still has a role, but it has to earn it every year.”

Marketing and risk management: Discipline over prediction

Volatility driven by weather scares, geopolitical headlines and fund activity can still create short‑lived pricing opportunities—but only for those prepared to manage risk thoughtfully. As a result, many producers are focused less on predicting market highs and more on establishing guardrails that help protect margins when uncertainty accelerates.

In that context, tools such as forward contracts, futures and options are often discussed as part of a broader risk‑management conversation. Options are viewed by some producers as a way to maintain flexibility—helping define downside exposure while keeping the door open to weather‑driven rallies if they emerge. In areas where basis remains historically strong, separating basis decisions from futures pricing has also helped producers respond more nimbly to local conditions.

“When the crop is early and uneven, waiting for clarity can be costly,” Gilpin said. “Being disciplined helps preserve margins when volatility arrives.”

Price outlook: Balanced risks ahead

Looking ahead, wheat prices face both supportive and limiting factors. Weather remains the primary wildcard, especially during critical spring growth and early summer harvest periods. Quality issues—such as protein levels and test weight—could also introduce class‑specific price volatility.

On the bearish side, comfortable global supplies and aggressive competition from lower‑cost exporters continue to cap rallies. Domestic feed demand remains limited, and futures markets reflect that reality.

Early‑season stress does not guarantee lower production, but it does raise the probability of class‑specific surprises if quality losses or abandonment trim availability in key growing regions. Wheat’s role as a global food security crop ensures it remains sensitive to disruption. Unexpected production losses, export restrictions or logistical challenges could quickly tighten specific markets.

For High Plains producers, the takeaway is clear: Focus on controllable factors—cost management, quality and disciplined marketing—while staying flexible in response to changing conditions.

Serving the U.S. and the world

Across the High Plains, wheat remains foundational to agriculture and to food systems far beyond U.S. borders. This season’s challenges reinforce familiar truths: wheat rewards patience, preparation and perspective.

As producers move through spring and toward harvest, marketing decisions will require attentiveness not just to futures prices, but to basis, quality premiums and global signals. In a market shaped as much by demand nuance as by supply totals, thoughtful risk management may matter more than ever.

“Wheat continues to serve the U.S. and the world,” Gilpin said. “The producers who succeed are the ones who recognize that wheat is both a local crop and a global one.”

Ken Eriksen can be reached at [email protected].