Cotton’s resilience: A testament to High Plains farmers and the value supply chain

High Plains cotton producers have endured three brutal years of drought, extreme heat and stagnant prices that tested the limits of even the most resilient operations. Yet as the 2026 planting season unfolds amid persistent dry conditions across Texas and the Southwest, a modest price rally in futures markets—driven largely by speculators and short covering—offers a glimmer of hope.

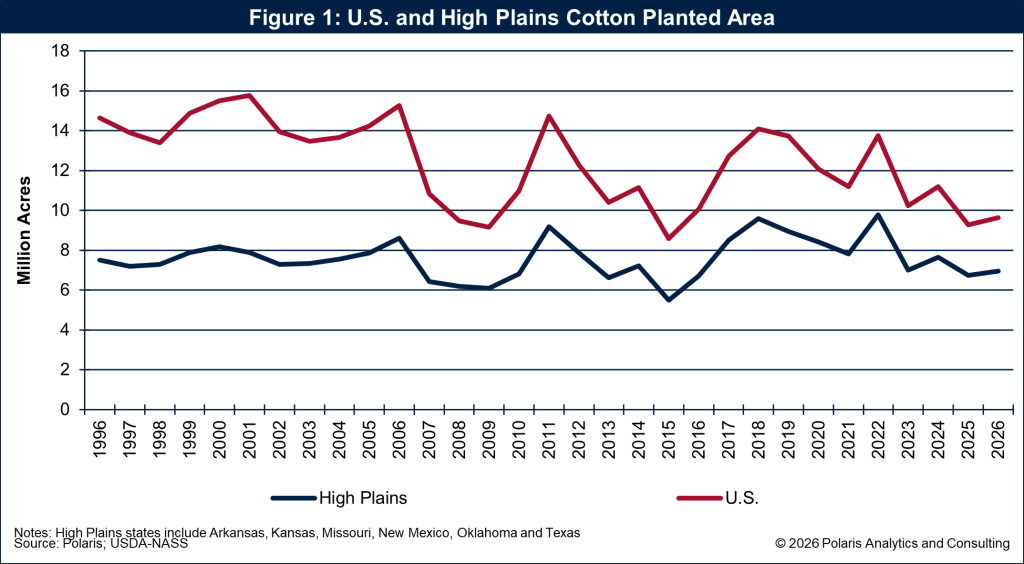

United States cotton planted area is projected to rise slightly to 9.64 million acres nationwide, up about 4% from 2025, according to U.S. Department of Agriculture’s intentions, with some upticks in the High Plains to 6.95 million acres from 6.73 million (as shown in Figure 1) as growers respond to relative crop prices and lingering optimism.

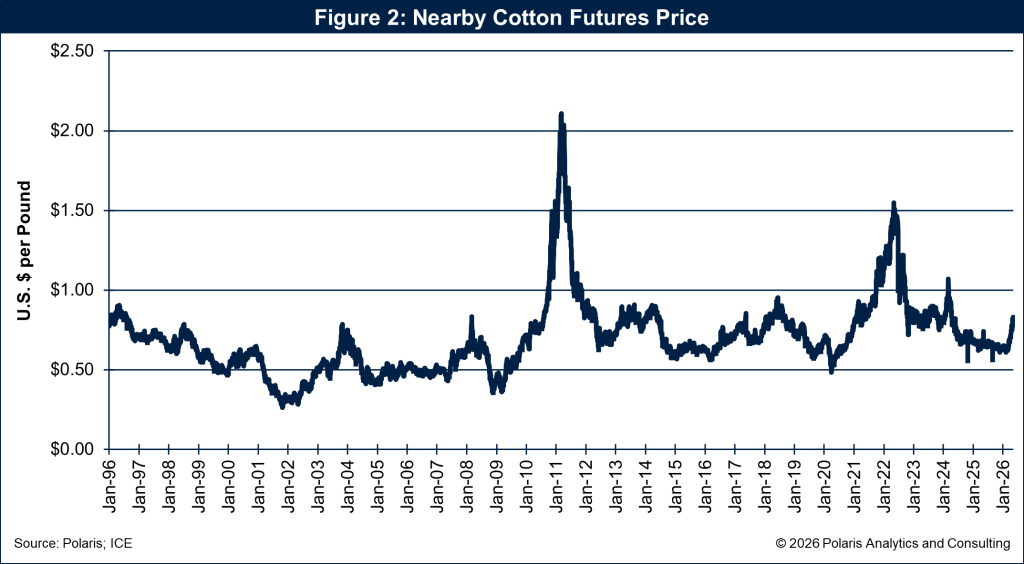

The past 16 months brought historically low prices and terrible marketing conditions, but the recent surge in ICE cotton futures (climbing from the mid-60s cents per pound into the low-80s in recent sessions as depicted in Figure 2) signals shifting sentiment. (At top photo courtesy of Esin Deniz, Adobe Stock.)

Headwinds remain formidable: Higher fuel and fertilizer costs exacerbated by geopolitical tensions, including the war with Iran; intense competition from Brazil; and ongoing infrastructure contraction in the ginning sector. Still, industry leaders see opportunity looming—if the U.S. can leverage its strengths in the farm bill, robust futures markets and potential policy wins like the Buy American Cotton Act.

Kevin Brinkley, president and CEO of Plains Cotton Cooperative Association, captures the raw reality facing growers. A grower-owned marketing cooperative serving Texas, Oklahoma, Kansas, and New Mexico, PCCA has watched its members navigate weather disasters and economic pressure.

“The 2025 production year had a decent crop compared to the previous three years—all under weather pressure,” Brinkley said. Disaster assistance programs, including Emergency Commodity Assistance Program and Farmer Bridge Assistance Program payments, have provided some relief, but fall short.

“Farmers are still looking at $100 to $150 per acre losses,” he said. “We’ve had ad hoc payments every year since 2017. What is the sustainability of that? It’s hard to live that way.”

Water scarcity compounds the pain in the High Plains, where irrigation is often supplemental. “Look at water tables today versus 20 years ago,” Brinkley explained.

Farms are pumping less due to higher electricity and fuel costs, leading some to plant only half or a quarter of irrigated land or switch to skip-row and drip systems. Balance sheets have taken a beating, with some land being turned back to landlords and producers contemplating exit.

“Farmers are not down and out, but close to it,” he said.

On the brighter side, Brinkley sees potential tightening in the global balance sheet. Brazil faces its own challenges—lacking the economic support and hedging tools U.S. producers enjoy—and a poor crop there could echo the supply crunches of 2008-09. Polyester competition from low-priced synthetics has hurt demand, but microplastic concerns could help cotton claw back market share.

“If we consume 500 million bale equivalents worldwide, with 120 million in cotton, just 1% shift from poly and nylon means another 3 to 4 million bales,” Brinkley said.

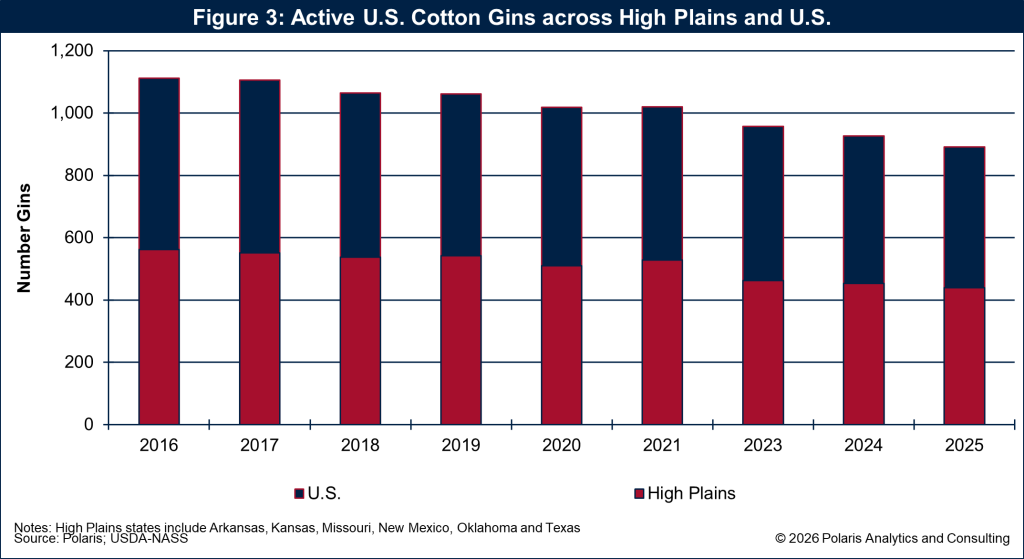

Ginning infrastructure tells a parallel story of contraction and consolidation as reflected in Figure 3, dropping 20% across the U.S. between 2016 and 2025 and 22% in the High Plains. Larger, more efficient gins have been built in Texas, but overall numbers continue to shrink through mergers, acquisitions and closures. “Once the infrastructure is gone, it’s gone,” Brinkley warned. “There are no programs to protect gins. Margins will get smaller, but something like BACA could help.”

Tim Price, executive director of the Southern Cotton Ginners Association, echoes the urgency of rethinking the industry’s future. Representing gins across Arkansas, Louisiana, Mississippi, Missouri, and Tennessee, Price has a front-row seat to the infrastructure erosion.

“We’ve gone from more than 300 gins to about 100 today,” he said. “Profitability of cotton impacts marketing. We lost infrastructure in the process.” Farmers adapted by relying on larger equipment and contract services, but that shift squeezed out smaller operations.

Price is blunt about competitiveness. “We get comfortable with government support rather than making solutions for long-term profitability.” Global rivals like Brazil bring new land online with fewer regulations, while U.S. trade policy has focused more on tariffs than fundamentals.

“We are not going to compete with a Brazilian farmer on cost,” Price argued. “We have to rethink—think differently. Focus more on demand and less on supply.”

The Buy American Cotton Act offers one path forward. The legislation, introduced in May 2025 as S. 1919 and in January 2026 as H.R. 7230, would create a domestic cotton consumption tax credit to incentivize U.S. fiber use in imported apparel and goods. “It’s been two years in the making,” Price noted, with strong response from retailers and bipartisan interest. “For every X of cotton imported from country Y, that country gets a tax credit if they use U.S. cotton.” Implementation would take time, likely through budget reconciliation, but it could bolster the full supply chain.

Coors Arthur, senior vice president at HTS Commodities (a division of Hilltop Securities), brings the trader’s perspective to the conversation. After 16 months of stagnant prices, the recent surge has been notable. “Fundamentals matter, but speculators drive the show,” Arthur said. Large speculators (managed money) had built the largest net short position in history before shifting to net long through buying and short covering, as shown in recent CFTC Commitment of Traders data. This financial activity, combined with macro factors like higher crude oil prices, has propelled futures higher despite uneven physical demand.

“OTC trading—over-the-counter, meaning customized bilateral contracts negotiated directly between parties rather than on the exchange—has stayed active under the radar, keeping the industry moving,” Arthur explained. For example, a merchant might lock in an OTC forward purchase with a mill at a fixed basis to futures months in advance, providing price certainty and flexibility that standardized futures cannot always match. “It’s keeping physical cotton flowing even when exchange volumes fluctuate.”

Brazil’s rise as an export powerhouse is real, Arthur acknowledged, but the South American giant lacks the U.S.’s robust support systems, futures markets and disaster aid. Higher global input costs from the Iran conflict hit Brazilian producers harder. “The U.S. is better able to absorb them,” he said. Meanwhile, polyester’s dominance has been challenged by sustainability concerns and shifting apparel production away from China toward lower-cost nations in South and Southeast Asia could create new demand avenues if paired with policies favoring U.S. cotton.

Despite the headwinds, the story of U.S. cotton remains one of resilience. Farmers continue to innovate with technology, precision irrigation and adapted equipment. Gins are right-sizing—consolidating into fewer, larger, more efficient facilities that can better serve export markets. The U.S. retains advantages through farm bill tools, marketing assistance and a consumer base that values domestic fiber.

BACA could be a gamechanger if it gains traction in Congress, potentially adding acres and revitalizing the supply chain from farm to retail. “It won’t happen overnight,” Brinkley noted, “but it might add acres and move us up to traditional levels.”

As one leader put it, the seismic changes in production agriculture demand fresh thinking. Farmers love to farm, but profitability is non-negotiable. With 2026 intentions showing cautious optimism and speculators injecting energy into prices, the value supply chain—from High Plains fields to global markets—stands ready to prove its enduring strength.

Ken Eriksen can be reached at [email protected].

Plains Cotton Cooperative Association

Formed in 1953 and headquartered in Lubbock, Texas, PCCA is a farmer-owned marketing cooperative serving growers in Texas, Oklahoma, Kansas. and New Mexico. Member-owned gins and producers rely on PCCA for innovative marketing programs, risk management and value-added services. The cooperative also operates The Seam, a leading electronic trading platform for U.S. cotton, and provides technology solutions to enhance gin efficiency.

It’s mission: Enhance profitability of grower-owners through collective strength in domestic and international markets.

Southern Cotton Ginners Association

Established in 1967, the Southern Cotton Ginners Association is a nonprofit representing cotton gins in Arkansas, Louisiana, Mississippi, Missouri and Tennessee. Led by Executive Director Tim Price, it focuses on safety training, legislative advocacy, technology adoption and member support. The association hosts the annual Mid-South Farm and Gin Show and collaborates with national groups to address industry challenges, from infrastructure preservation to policy issues affecting ginning profitability.

HTS Commodities – A Division of Hilltop Securities

HTS Commodities, part of Hilltop Securities, provides tailored futures, options and over-the-counter trading solutions for agricultural producers and commercial clients. With offices across the U.S., including a strong cotton desk in Memphis, the firm combines decades of hedging expertise with institutional backing. Senior Vice President Coors Arthur, a cotton specialist with global experience, helps clients navigate volatile markets through proprietary strategies and compliance-focused risk management.

Related Articles